FinTech Isn't Dead

Fintech has not been ‘hot’ in venture for a while, but: 1) It is the largest revenue opportunity by industry; 2) It will be around forever; 3) It touches every vertical, from health to climate; and 4) It is (relatively) unloved at the moment. Point (4) is actually a good thing.

Over the past few months, I’ve gone deep into verticals across finance and although there are several areas that I’m excited about, I want to start with the five below.

If you are a founder building in any of the domains, please reach out.

1) B2B Payments & Vertical ERPs

It’s common knowledge that the global B2B market is large: $125T. Although the perceived TAM is enormous, it doesn’t paint a fair picture of the opportunity set and what it takes to win.

I believe that the ‘payment’ – largely facilitated through checks, credit, ACH, or virtual cards – is the less complex piece. However, the mechanism through which payments are made (for example, >50% in the US via checks) and the customized workflow needs that predate a payment are where the pain point resides.

The opportunity, therefore, is in vertical ERPs (VERPs) - vertically focused companies, workflow-specific platforms that offer a payment layer, along with SaaS that runs the workflows. Within these platforms, feature sets include: matching payment orders, calculation and withholding of correct taxes, customized approvals within an organization, executing pay-outs in bulk, reconciliation with the general ledger, and ERP/accounting integrations, among others. The best vertical ERPs embed the best practices and assumptions of a specific vertical. Examples include Nickel for construction and Ontic for physical goods suppliers.

There is a stark contrast between vanilla vertical software and VERPs. The key difference is that with VERPs, there is financial functionality. The most effective VERPs are those that are ‘touching’ the cash flows of a business. That said, the primary GTM for a startup must remain workflows - which can then translate into customer loyalty - with an eventual mission to embed into cash flows. Payments is an easier sell given the core need. Still, with time, corporate cards are more lucrative as VERPs can earn interchange by issuing the card, revenue via payment facilitators, and monthly SaaS for workflows.

Given the sheer scale, this is not a winner-takes-all market; at present, Square, Bill, and Toast all operate as full-service public companies. Unbundling Bill.com in a visual mechanism to envision what the future looks like – they only cover <2% of businesses in the US and don’t scale well as the SMEs grow into more complex organizations.

In summary, what a winner looks like:

ERP integrations are paramount to solving quicker workflow problems (NetSuite is the market leader in the US today).

Enabling AI agents into workflows can allow for a less manual process and quicker reconciliation.

Where Bill.com lacks is the ability to grow with organizations and offer more horizontal features at scale, like currency management and working capital.

Begin with payments, with an eventual vision to ‘touch’ cash flows through working capital financing and corporate cards, among others.

I would be excited to see general ledger data being used for embedded lending, too. The goal is to create as much unification across an organization as possible.

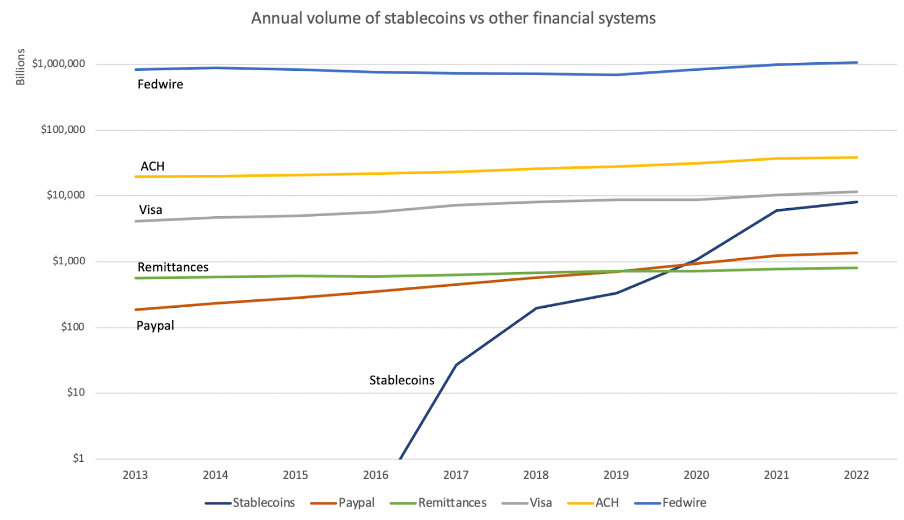

2) Stablecoins

Although stablecoins have been around for a decade, I feel strongly that we’ve reached a ‘why now’ moment with the asset class. Many associate stablecoins with crypto, but I instead view it through a different lens and more so linked to a very strong use case of blockchain (immutable ledger) technology.

We’re seeing the convergence of traditional finance and crypto happening, and stablecoins will be the beachhead. From a regulatory perspective, the US could pass HR 7466 (The Stablecoin Trust Act), which aims to legitimize stablecoins by ensuring adequate levels of liquidity for issuers and scheduled audits. In Europe, the Markets in Crypto-Assets (MiCA) regulation has already been passed and will be implemented in full by early 2025. I believe the US has a vested interest in passing a stablecoin law, as this maintains demand for the USD across foreign markets, which allows them to service their growing debt.

In terms of use cases that we’d see across companies we want to back (not exhaustive):

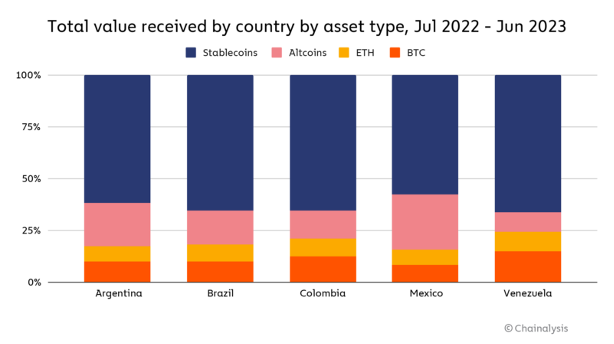

Real-time settlement: We’re seeing this with Vance, where they’ve processed a growing proportion of remittances via stablecoin rails. This has enabled them to create 80%+ margins for themselves vs. SWIFT, given it’s cheaper, faster to go through stables, and completely traceable. PayPal also introduced PYUSD, which is their stablecoin pegged to the USD; it’s used widely and enables instant settlements / cheaper cost of selling cross-border for users. We’ll see similar use cases being applied by companies in payments, payroll, and reconciliation.

Store of value: In developed markets, we frequently cite Bitcoin as a store of value. In markets with high inflation and unstable governments, the demand for a self-custodial, stable currency is sky-high. The Rupee depreciates 3-5% annually, but the citizens of Venezuala don’t have it so good.

Automatic ledger: The majority of problems in financial services can be distilled down into two areas: identity and reconciliation. The $85M ledger mismatch we’re seeing in Synapse / Evolve’s case is purely due to two separate stakeholders maintaining two separate ledgers. Stablecoins can adequately be used as a settlement layer—abstracted away from UX—given that they are an ‘automatic ledger’ as they’re hosted on a blockchain.

A winner operating in stablecoins will be less specific and more unpredictable. The use cases above are illustrative, and they will continue to evolve especially as regulation gets firmed up. Stripe is leading the way with digital stablecoin acceptance, and there is room for companies to do the same for offline use cases. I believe that ‘Phase 1’ of stablecoin companies will abstract away the complexity around stablecoins, to simply benefit the user without the user knowing it (what Sling, Vance, Mural Pay, amongst others are doing today). ‘Phase 2’ will begin when stablecoin use is more normalized and behaves as the front-and-center of a company’s offering, as we are seeing with orchestration-led and - recently acquired for $1.1B - Bridge.

3) Financial Crime

Fraud is an epidemic in financial services. In 2023, in the US, incidents where data was compromised increased by 78% compared to the year prior. Research from the House of Commons (2019) indicates nearly $2T gets lost through money laundering and crime annually. Most surprisingly, a research paper from 2020 concluded that criminal enterprises retain 99.95% of the proceeds of crime.

Although fraud is already the largest issue for compliance teams, I envision it to become a problem of even greater magnitude in the future. This will be driven by sophisticated AI-led attacks that will incorporate ‘deep fakes’ to bypass identity verification systems. We’re seeing larger ‘incumbent’ fintechs go heavily on the defensive. Recently, Monzo introduced a host of features to combat fraud, some of which include operating in ‘known locations’, trusted contacts, and daily allowances by use case. There’s the saying, “with faster payments comes faster fraud”. What’s separately true for finance and why attacking fraud is paramount: the downside of a ‘bad’ user is not zero, it’s negative, as you can lose funds.

Regulation – usually a lagging indicator – has shown an increase in emphasis on consumer protection. Comparing The Payment Services Directive 2 (PSD2) to PSD3, the latter has enforced more stringent customer authentication requirements such as biometrics, with no exemptions for low-risk transactions (as was the case with PSD2). Additionally, with PSD3, data encryption is a bare minimum, and financial institutions must engage in incident reporting instantly as opposed to fixed deadlines.

Given the scope of the pain point which is financial crime, the opportunity is vast. I’ve listed out key areas where fraudulent activities generally occur, and will use this as a benchmark to unpack where we can find opportunities:

- Account Opening:

The primary root issues here are identifying the right individuals and verifying documents.

Given the sophisticated AI-led attacks we will continue to see, there is an opportunity to work with companies that can decipher deep fakes instantly while triangulating reasoning through device behavior, visual distortions, and masking of audio, among other cues.

Similarly, for document verification, the nature of image-editing tools is only getting better. Therefore, there’s a sufficient willingness to pay from customers to reduce fraud but also lower the manual review time. We will find companies that use computer vision to analyze visual elements on documents, optical character recognition (OCR) technology to rapidly compare text-based data, and systems that allow for cross-document verification. We’ve seen proof points of generative adversarial networks reducing false positives in handwritten checks by 90% already; although early signs, this is indicative of the opportunity set for AI-led solutions.

- Transaction Monitoring

Once an account is opened, the next – and most critical – phase of managing fraud is real-time transaction monitoring. This is an incredibly convoluted problem, especially in the context of the different incentives across the ecosystem. For example, the last thing merchants want is ‘false positives’, where a user is blocked that shouldn’t be blocked, while at the same time, banks want to be more risk averse. Winning companies will tread this balance carefully.

As is the case with document verification, I remain excited about AI-led use cases that sit on top of transaction data. The ‘ideal’ company will track various forms of fraud: layering (ensuring the root entity transferring funds has good intentions), political affiliations (validating that politically exposed people are not money laundering), and mules (ensuring that a ‘mule’ is not being used to transfer funds on behalf of a fraudulent party).

The root issue in transaction monitoring today is that data lakes are siloed. Banks, payment schemes, and merchants all have their own ‘worldview’ of a customer. A winning company will therefore find ways to collaborate across stakeholders, globally, to form the most accurate picture of a customer.

- Ongoing Compliance

Startups operating in this realm will come into play after a transaction is flagged. For example, they will evaluate whether a customer's ‘chargeback’ is legitimate or fraudulent.

Winning companies here complement the transaction monitoring services above, with an emphasis on maintaining data encryption standards as third-party data is transferred in/out and tokenizing sensitive data across stakeholders.

It is unclear whether a vertical focus like Identity (as shown in Onfido and Alloy) is the best path to market, or whether it’s better to sell full stack to banks (Sardine, Flagright). There is merit to both, but what remains a non-negotiable is the ability to be an ‘open network’ and allow for integrations through the product workflow.

4) Embedded Finance

Embedded finance involves distributing financial products through non-financial companies. It’s the mechanism of bringing banking to where customers already are. The case for offering financial products for non-banks is driven by the strength of proprietary data. For example, AirBnB (notable insurance product, AirCover), Uber, Shopify, and Toast are platforms that have amassed specific, behavioral datapoints on users, and can leverage this information to successfully underwrite a customer.

Broadly, sponsor banks, BaaS providers, and end-brands are the main stakeholders within embedded finance. However, the ecosystem that enables a customer to borrow funds through a non-bank platform is convoluted and privy to a host of different roles:

Merchant Workflows: This includes platforms, by verticals, that merchants engage with; Flexport for freight, Shopify for e-commerce, and Nickel for construction. Startups in this category are customer-facing and workflow-focused.

Credit Providers: These are not financial institutions themselves, but act as conduits to deliver capital to a merchant’s customers. Notable startups that play this role include Airbase, Billie, and Pipe.

Underwriting Platforms: Companies like Alloy, Zest AI, and Lendflow use data science to provide better risk management and decisions for credit. The primary role played here is to ingest data and provide an output, that is sent to credit providers (above) in the value chain.

Unified APIs: These tools are developer-facing, and make it easier to integrate with service providers within a certain domain. Notable startups here include Plaid for financial services, Twilio for telecom, and TrueLayer for open banking.

Data Aggregators: They form the foundation of the embedded finance value chain. Each company plays a ‘mini role’ in forming a complete picture of a customer requesting a financial product. These roles fall into buckets such as fraud (Sardine), AML (unit21), KYC (Trulioo), cash flow (Heron), and accounting data (Xero).

As shared above, the value chain is complex to enable embedded financing. In tandem, given the number of solutions, there is always an opportunity to work with founders across the ‘stack’. I am personally most excited about startups focused on underwriting (using credit history, transaction data, government records, and alternative inputs) and vertical-led workflow solutions.

Embedded finance is a unique beast in that the opportunity segment is both fragmented and deep. Use cases span across e-commerce with BNPL, instant credit as form factors, but also other verticals like mobility (EWA for drivers), real estate (mortgage financing), fitness (personalized health insurance based on activity), and supply chain financing, among others.

5) Using Agents & LLMs

The current platform shift in AI will positively impact financial services. From my perspective, the two broader use cases will be derived from workflow agents and LLMs specific to finance.

a) Agents must perform three functions to be deemed effective: 1) they must be able to perform and complete an action; 2) memory repositories should be in place to recall actions they’ve taken; 3) there should be in-built mechanisms to error correct and critique actions performed along the way. Below are examples of how workflow agents can be implemented in fintech:

Financial analysis: using agents to evaluate SEC documents, filings, and financial models to provide a complete picture of the ‘health’ of a company. We can see use cases of agents complementing the work of research or investment banking analysts.

Automated debt collection: An extension or v2 of TrueAccord, where agents can follow up with customers and interact with authorities to set in motion a cost-effective and stringent process to recoup funds for companies.

KYC / KYB: Arva is an example of agents being used as KYB analysts to verify a businesses’ activities, ownership structure, etc, to provide a cheaper and faster way for compliance teams to offer onboarding to customers. Greenlite is another example of doing the same for document processing and fraud checks.

Chargeback for Merchants: For credit or debit card companies, whenever a customer issues a chargeback, the merchants have to manually submit evidence to fight the claim. Companies like Coris are creating agents that understand the context and fight claims automatically.

Accounts Receivable / Payable Automation: The use of agents to correct invoices before they are sent to broader teams and facilitate collection from clients, with the primary goal of reducing days outstanding for accounting teams. Companies like Stuut are an example of a startup operating in this domain.

The list is extensive; other use cases include using agents to track fraud through transaction monitoring, working within wealth firms for quicker client onboarding, customer support for non-finance companies to lower their cost of embedded finance servicing, automating claims for health insurance, and collecting customer data while analyzing loan repayment risk for credit firms, among others. The above examples are predominately ‘single tools’, where agentic behavior is optimized for a single use case. The reality is, that much of financial services is highly all-encompassing, and the major issues we’ve witnessed in the past are driven by siloed data. Therefore, the form factor for exciting use cases falls into two buckets:

- A Multi-Agent System: Single tool agents collaborate and amplify their use cases. Think of it as an ‘agent workforce’; a parallel being Relevance AI, but for financial services. Single tools report back sequential behaviors and learn from them, while in Multi-Agent systems, these agents will communicate directly with each other, learn and problem-solve collectively, and grow to tackle much more complex asks.

- Low Code or No Code ‘Tools-As-A-Service’: ‘Toolboxes’ that offer off-the-shelf agentic workflows for customers. The large benefit here is no restructuring of code will be required to implement agents at scale. Monetization for companies here will be driven by unified API calls or traditional SaaS pricing. (Unified API calls that go deep into integrations – Codat, integrating with 19 accounting platforms and 16 commerce platforms).

We will see single-agent companies, but personally, if founders don’t have a path to multi-agent systems, I feel it will be limited – both from the perspective of its user experience, but also for developers managing their codebase, as agents need to keep having to be re-initialized as new tasks are encountered.

It is not all rosy - we will see challenges as it relates to adoption. For one, the cost structure must make sense for companies. If the compounding cost of API calls to engage with agents is greater than the problem itself, sustained implementation will fail. Similarly, and to my prior point, more modular and set-in-stone feature sets must be rolled out, and constant re-initializations are inefficient and costly for companies.

b) The second opportunity segment is customized LLMs for financial services firms. Gen AI is a natural opportunity within fintech, given the vast amount of siloed, unstructured data that has been created within organizations. There is so much information, but it’s difficult for large companies to make meaning of it.

As it relates to the kind of LLMs, there has been immense progress for general-purpose models, but the hit rate is far from where we want to be; Princeton’s SWE Paper shows a 12% success rate with GitHub issues vs. 3.8% with retrieval augmented generation. GitHub issues being agnostic is a primary proxy for the lower hit rate, and more focused models that have been fine-tuned – like Hugging Face’s FinBERT – are much more reliant.

Large foundational models with the highest parameters do have the highest quality of output, but they are not specific enough. Given the unique needs of financial organizations, customized LLMs are more attractive, and each segment can offer its own ‘weighting’ within each neural network to offer the best solution. There are a host of other advantages of operating within customized models. One example is the ability to initiate automated unified API calls within the model, which provide deep data integrations; a case-in-point is Codat’s focus on banks and their multitude of integrations across accounting and commerce platforms.

There is one caveat for implementation. In the case of any regulated industry, my personal choice would be to invest in companies that take a more co-pilot approach, given hallucinations in models and the stringent need for accuracy in financial services. Companies like Hyperplane live by this mantra and built their product around this notion. They use first-party customer information and provide banks with insights into their user base at the micro level, within the confines of a private LLM. There is no information sharing with banks, and customer data stays within the boundaries of a company. Hallucinations are not keeping them up at night, as insights are broadly internal, and there is a human in the loop to oversee any major decisions guided by those insights. Other examples of taking a co-pilot approach are Materia for accounting and Quimis for insurance claims.

Given the fast-moving nature of developments in AI, the opportunity segment within fintech is evolving. What remains unchanged is the degree of unstructured data and the high cost of servicing in finance. Therefore, the above points are not all-encompassing, and we will see models that will surprise us in terms of form factor and scalability.

Thanks for reading. Feedback always welcome - shoot me an email!

Hi Akshay! Super-interesting deep-dive. I think the area for most potential are Agents and LLMs for compliance and financial crime infrastructure. Startups building RegTech solutions for use cases like KYC, RBI Regulations and DPDP have potential as regulatory load is increasing for companies. Furthermore, specific sectors such as India's hotel industry are facing issues with data protection agreements due to Personally Identifiable Information (PII) such as travel data. Financial crime infrastructure such as compliance with the tax and money-laundering regulations are growing for companies as well because of the need to reduce risk and ensure compliance efficiently. I have been delving deep into the RegTech sector. Would love to connect with you to exchange views!

I write a newsletter focused on analyzing and identifying investment opportunities in the LegalTech sector. I've written a post analyzing the three whitespaces to look out for in 2026.

https://harshithviswanath.substack.com/p/three-legaltech-whitespace-plays

Sold read thanks!