Chasing Black Sheep

Revolutions, reflexivity, and talent dilution.

Early-stage investors don’t have the luxury of knowing any company as well as its founders do. Founders are in the weeds, obsessed with their ‘baby’, while investors spend a fraction of the time thinking about a single company. But that very constraint provides investors with breadth: a 10,000-foot view across domains and geographies, and days spent forming a sense of the ‘lay of the land’.

With the benefit of this panoramic view, one thing has become clear to me: always follow outlier talent. It’s the earliest indicator of where the next technology revolution is forming.

Of all the variables that determine whether a company succeeds, the founder is the constant. I’ve gone into rabbit holes on markets, business models, and narratives, and often come away surprised by the out-of-distribution entrepreneur that changes my perspective completely (which is why I previously wrote this). The best investments I’ve seen begin with a founder operating in a domain that was unexplored by the fund, backing an idea that didn’t fit any existing framework. The type of founder who selects a domain because of technical promise, not capital availability.

But simply chasing talent comes with its own set of caveats. Not all talent clustering is equal: during a bubble, a sector gets flooded with smart, credentialed people chasing capital, and that group can look, on the surface, indistinguishable from the early believers who were there before the narrative took hold. To understand this better, I think it’s helpful to consider how technology cycles evolve and how talent clusters form and move with time.

Cycles and Reflexivity

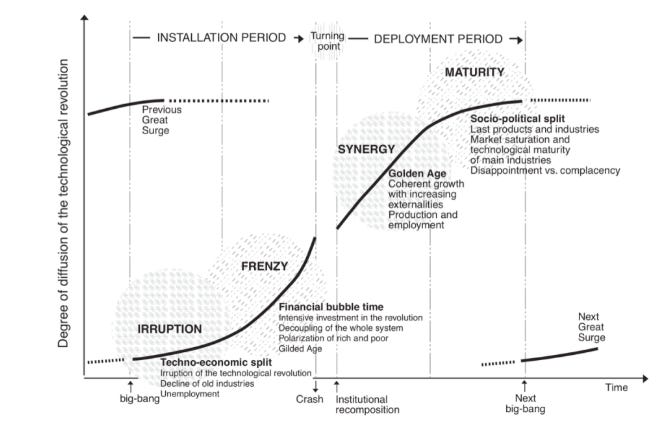

Venture nerds are aware of Perez’s seminal book, ‘Technological Revolutions and Financial Capital’. In it, she neatly lays out four distinct phases of a technology cycle:

Irruption: The big bang, where “the universe of possibilities inflames the imagination of young entrepreneurs”.

Frenzy: The new technology becomes mainstream; the phase of “intense exploration of all the possibilities of the technological revolution, through bold and diversified trial and error”.

Synergy: The golden age, where financial capital and the development of technology work in tandem.

Maturity: Saturation leads the way, cracks begin to show, and the old technology paves the way for the next wave.

Perez’s view might be too academic, where in reality, narratives take on a life of their own. It takes me back to when my Dad handed me George Soros’ book on reflexivity. The core idea has stuck with me: prices don’t merely reflect fundamentals, they shape them. For example, the ‘frenzy’ period persists for longer than is expected, as any contradictory evidence towards the technology is simply ‘par for the course’. Let’s take crypto from ‘17 to ‘22: every crash was a ‘buying opportunity’, every failed ICO part of the ‘early innings’ narrative, every regulatory threat proof that the instrument was disrupting the establishment. We see reflexive tendencies and the same loop with talent: talent attracts capital, capital bolsters the narrative, enabling the narrative to develop its own immune system, eventually leading to a bubble.

And these reflexive dynamics don’t just play out once per revolution. Within a revolution, there are ‘mini cycles’, too. For example, since the 2000s, we’ve seen inflection points for mobile, cloud, crypto, and now AI. Each of these platform shifts have their own ‘mini cycle’ of irruption, frenzy, synergy, and maturation. To some degree, each mini-cycle is a nested reflexive loop, and they run at different speeds from the master cycle (IT revolution) that Perez describes. Cloud and mobile were steady; narratives and fundamentals were roughly in sync. Crypto, the opposite, where the story far outpaced production. AI is split: the infrastructure demand is real, but the application layer is awash with ‘AI-native’ and ‘agentic’ as vocabulary for capital attraction.

This overextension of a narrative impacts the type of entrepreneur within each cycle phase. The economic bubble sets the foundation for social consensus, where the volume of builders rises, but the signal falls. Social consensus brings more capital, capital attracts higher salaries, and salaries bring ‘MBA creep’ and incrementalism. The people who were there at the irruption (the researchers, the obsessives, the ones operating at the fringes before anyone else cared) might have just moved on.

This unpredictable nature of mini-cycles, the strong reflexive loops, and the role of narratives make our world of technology far more unpredictable than it’s made out to be. And it brings me back to the single variable that guides me.

Following the Fringe

If cycles and crystal balls to predict market timing are a fool’s errand, then what can help us lead the way? For me, it’s where the most out-of-distribution people are spending their time.

The qualities shared among this group - ‘irruption-phase’ talent - could become its own post, but at a surface level: the unwillingness to be deterred by consensus norms or advice, the courage to go deep into rabbit-holes with no goalpost or dopamine hit in sight, and an independence of thought that is core to their identity. In first meetings with this group, I often feel uncomfortable and even perplexed by how they’ve spent their time; I’ve now learnt to treat this as a positive signal. I’ve seen this pattern play out in my own journey, whether it was Parth’s conviction that stablecoins should form the foundation of Aspora’s product in early ‘22, or Rodri’s pivot from NFTs into agentic infrastructure at Crossmint, just as the AI revolution took flight. Often, the ‘winners’ of a cycle - upon closer look - have long been obsessing and studying the craft of the technology for years prior. If we look to today, consider Demis Hassabis: his obsession with building intelligent systems began at 17, when he was lead programmer on the adaptive AI game Theme Park, a thread he continued to pull on through a neuroscience PhD, before co-founding DeepMind.

The quality and character of talent in a sector, therefore, becomes a diagnostic tool. During ‘irruption’, it’s the early believers, researchers, and people operating at the fringes. This is where early-stage investors want to spend time. During the ‘frenzy’ phase, although there is a crowd, talented entrepreneurs arrive to commercialize. A tell here is that when most pitches cover similar source materials and memos, the cycle has moved - still a great moment in time for investors, as first-movers are not always winners. But by ‘synergy’ and ‘maturity’, the outliers have solidified their status or have moved on, with growth capital taking centre-stage and adverse selection setting in. The idea then is to follow the talent, while knowing where we are in the cycle. For example, looking at the present, if all investors are focused on companies building in AI, there’s a possibility of completely missing the next irruption. Chances are that there is a group of highly promising founders who have moved on or are utilizing AI in the most unique possible way.

Which is why being thesis-first, geo-led, or industry-focused as a fund - while it gives LPs the comfort of putting you into a ‘box’ - constrains the aperture at exactly the moment it needs to be wide. The next irruption is unlikely to come from the domain you’ve pre-committed to. Keeping an open mind and trusting outliers, even when the idea feels uncomfortable, is how you catch lightning.

There’s no silver bullet for finding the next irruption. But there is a muscle I try to exercise: spending time at the extreme fringes, long before they feel like opportunity. Admittedly, far easier to state than to actually act on. It could mean reading Satoshi’s Bitcoin paper in 2008, when crypto meant nothing to most people. Or sitting with AI researchers before GPT, when the field was an academic backwater. Or understanding why a handful of researchers are obsessed with synthetic biology, despite the field having disappointed investors for a decade.

That said, not every idea at the fringe must be original. Sometimes a ‘mini cycle’ can breathe life into models that failed before their time. Uber thrived because of the iPhone and the proliferation of GPS; Webvan failed miserably in the dot-com era, but Instacart works like magic. Investing in AI before 2017 would have borne no fruit; today, the same ideas are building generational companies. This is not to suggest that market beats talent, but rather outlier talent shows up when a previously-failed model becomes viable, because they can see the substrate change before consensus does.

Often, the reflex when meeting a ‘black sheep’ founder – someone who stands out too far from the crowd - is to dismiss them. The ideas feel too crazy, too early, too distant from the consensus. It might even unsettle you. But I’ve learnt to take a closer look. It might just be the early signs of the next irruption.

Thank you to Rahul Sanghi from Tigerfeathers for reading and editing my drafts.

Enjoyed reading this!

A corollary of this I've observed - usually in early phases of an emerging technology, you'll see a founding team that hasn't known each other 'for x years/long time'. Mostly because networks are disparate / or haven't existed for a longer time yet.

interesting read for sure, ! but i wonder if all black sheep / outlier founders have the same output, for example we mightve thought of VR in between as a big stage/ metaverse , but then it didnt go very far, and now a few palyers are alive, i am not saying they are wrong, but are they perpetually at the stage of irruption , a few could say the same for tech like crispr right?

i guess only a few forms of tech hit that takeoff velocity to get that steam and VC capital